Blog / E-Commerce Taxation in UAE vs. KSA

E-Commerce Taxation in UAE vs. KSA

E-commerce businesses in the UAE and Saudi Arabia face distinct tax environments. Here's what you need to know:

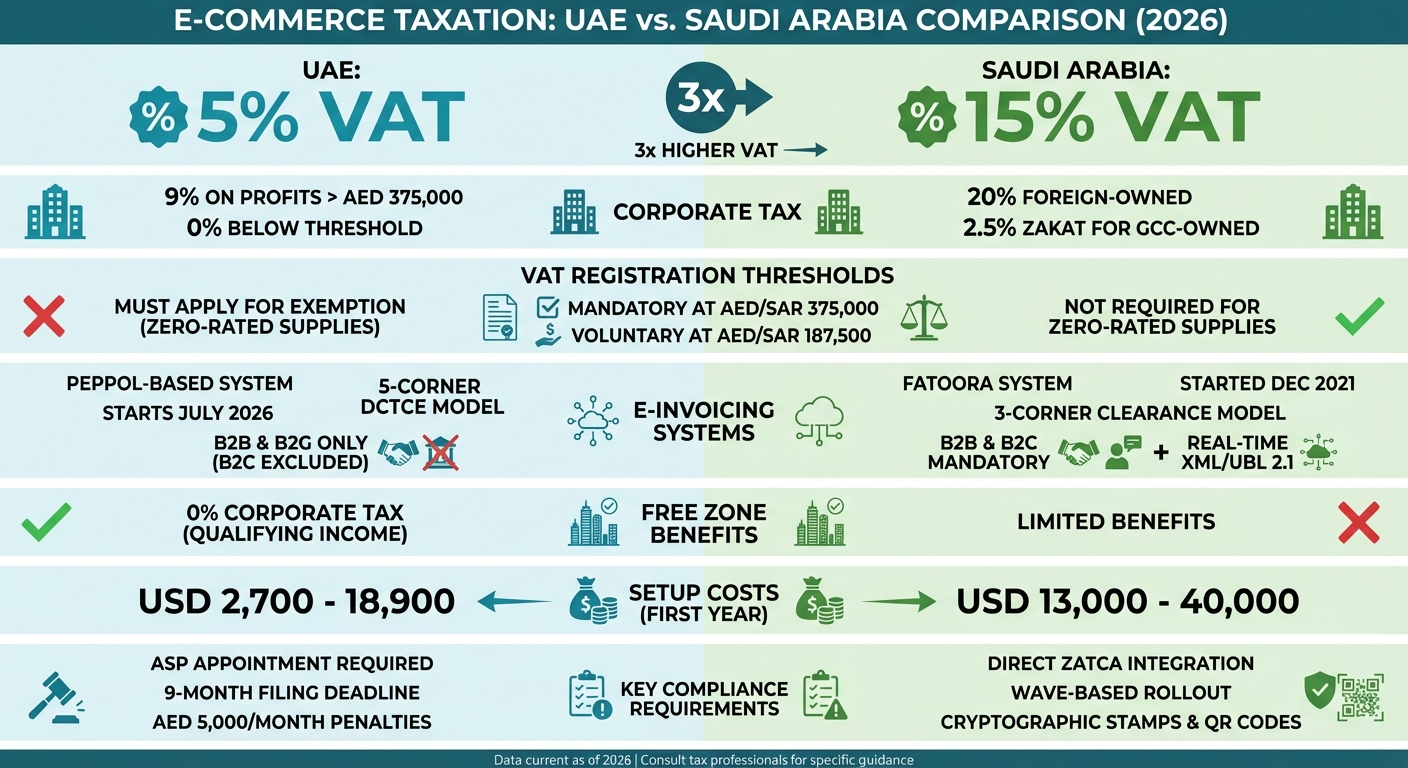

- VAT Rates: UAE applies a 5% VAT, while Saudi Arabia has a 15% VAT. This difference impacts pricing, profit margins, and competitiveness.

- Corporate Tax: The UAE introduced a 9% corporate tax (profits above AED 375,000) in 2023. Saudi Arabia imposes a 20% corporate tax on foreign-owned profits, with GCC-owned entities paying 2.5% Zakat instead.

- E-Invoicing: Saudi Arabia uses the FATOORA system, requiring real-time invoice clearance. The UAE plans to adopt a Peppol-based e-invoicing system starting July 2026, focusing on B2B and B2G transactions.

- Compliance Costs: Both countries require businesses to upgrade accounting systems to meet digital tax requirements, with penalties for non-compliance.

- Free Zones: UAE Free Zones offer 0% corporate tax on qualifying income, making them attractive for cross-border e-commerce.

Quick Comparison

| Feature | UAE | Saudi Arabia |

|---|---|---|

| VAT Rate | 5% | 15% |

| Corporate Tax | 9% (profits > AED 375,000) | 20% (foreign-owned profits) |

| Zakat | Not applicable | 2.5% (GCC-owned entities) |

| E-Invoicing Start | July 2026 (Peppol-based) | December 2021 (FATOORA) |

| Free Zone Benefits | 0% on qualifying income | Limited |

Understanding these differences is crucial for planning operations and ensuring compliance in these markets.

UAE vs Saudi Arabia E-Commerce Tax Comparison: VAT, Corporate Tax, and E-Invoicing Requirements

VAT Rates and Registration Requirements

5% VAT in UAE vs. 15% VAT in KSA

The VAT rate in Saudi Arabia is three times higher than in the UAE, giving UAE-based e-commerce businesses a clear pricing advantage. This difference significantly impacts pricing strategies, profit margins, and consumer behaviour in both markets.

For instance, a product priced at AED 1,000 in the UAE would include AED 50 in VAT. However, the same item in Saudi Arabia would be subject to SAR 150 in VAT (approximately AED 150). This forces businesses to rethink their regional pricing to remain competitive.

"The risk of double VAT errors can reduce margins. With the UAE VAT system at 5% and the KSA VAT system at 15%, a single transaction could result in non-recoverable input VAT and potential penalties."

Registration Thresholds and Exemptions

Beyond the rates, the registration requirements in the UAE and Saudi Arabia add another layer of complexity. Both countries share the same thresholds: businesses must register for VAT if their taxable supplies exceed AED/SAR 375,000, while voluntary registration is allowed for those above AED/SAR 187,500.

However, the treatment of zero-rated supplies sets them apart. In Saudi Arabia, businesses dealing solely in zero-rated goods or services are not required to register for VAT. On the other hand, the UAE mandates that such businesses formally apply for an exemption from the mandatory registration requirement. This distinction is particularly relevant for e-commerce businesses focused on exports or sectors like investment-grade precious metals, which are zero-rated in both countries.

| Feature | United Arab Emirates (UAE) | Saudi Arabia (KSA) |

|---|---|---|

| Standard VAT Rate | 5% | 15% |

| Mandatory Threshold | AED 375,000 | SAR 375,000 |

| Voluntary Threshold | AED 187,500 | SAR 187,500 |

| Zero-Rated Registration | Must apply for exemption | Not required |

| Record Retention | 7 Years | 10 Years |

These differences in VAT rates, registration thresholds, and exemption processes highlight the unique challenges businesses face in navigating these markets. They also set the stage for the upcoming digital invoicing requirements.

E-Invoicing Requirements: FTA vs. ZATCA

KSA's FATOORA System

Saudi Arabia's FATOORA e-invoicing system rolled out in two distinct phases. Phase 1, which began on 4 December 2021, required businesses to generate and store electronic invoices. Phase 2, effective from 1 January 2023, introduced direct integration with ZATCA's platform for real-time clearance.

The system relies on ZATCA-specific XML/UBL 2.1 formats for real-time processing. For business-to-consumer (B2C) transactions, simplified invoices include cryptographic stamps and QR codes for verification. ZATCA has implemented this integration through sequential "Waves", gradually targeting specific taxpayer groups based on their annual taxable revenue. As of early 2026, the system has reached Wave 11, progressively lowering revenue thresholds to include medium and small enterprises.

Meanwhile, the UAE has opted for a different path, adopting international standards to shape its e-invoicing framework.

UAE's Peppol-Based E-Invoicing

In line with the GCC's digital transformation goals, the UAE has introduced a Decentralized Continuous Transaction Control and Exchange (DCTCE) model for e-invoicing. The Federal Tax Authority (FTA) has embraced the globally recognised OpenPeppol standard, which simplifies cross-border invoice exchanges.

"By adopting a proven standard such as OpenPeppol, the business community has access to wider network where eInvoices can be seamlessly exchanged with businesses outside the UAE."

- Ministry of Finance, UAE

The UAE's system will roll out in stages, starting with a pilot programme on 1 July 2026. Phase 1 becomes mandatory on 1 January 2027 for large entities with annual revenue of AED 50 million or more. These businesses must appoint an Accredited Service Provider (ASP) from the Ministry of Finance's approved list by 31 July 2026. ASPs play a critical role, handling invoice validation, transmission to buyers, and near real-time reporting to the FTA.

Currently, the UAE's e-invoicing system excludes B2C transactions, VAT-exempt financial services, and certain international airline transactions. The government anticipates that proper implementation could lower invoice processing costs by around 66%.

E-Invoicing Systems Comparison

| Feature | UAE E-Invoicing (EIS) | KSA E-Invoicing (FATOORA) |

|---|---|---|

| Model | 5-Corner (DCTCE) | 3-Corner (Clearance/Reporting) |

| Standard | OpenPeppol | ZATCA-specific XML/UBL 2.1 |

| B2C Requirement | Excluded | Mandatory (Simplified Invoices) |

| Technical Security | Validation and encryption via ASP | Cryptographic stamps and QR codes |

| Reporting Timeline | Near real-time via ASP | Real-time (Clearance) or within 24 hours |

| Mandatory Start | 1 January 2027 (Phase 1) | 4 December 2021 (Phase 1); 1 January 2023 (Phase 2) |

| Non-Compliance Penalty | AED 5,000/month (system failure); AED 100/document (capped at AED 5,000/month) | Varies by violation type |

The technical demands of these systems vary considerably. In the UAE, invoices must be structured and machine-readable, ruling out unstructured formats like PDFs, Word documents, or scanned copies. Businesses are also required to ensure the accuracy of their master data for customers and suppliers, as errors could lead to rejections by the ASP or the Peppol network. Additionally, any system failures must be reported to the FTA within two business days to avoid a daily AED 1,000 penalty.

Comparative Analysis for the VAT Revenue Performance of UAE by Shamsa AlSalloum

Corporate Tax and Zakat Requirements

When it comes to e-commerce in the UAE and Saudi Arabia, understanding the nuances of corporate tax and Zakat is essential. These elements, alongside VAT and e-invoicing, play a major role in shaping profit margins and overall fiscal strategies.

The UAE introduced a 9% corporate tax on taxable profits exceeding AED 375,000 as of 1 June 2023. For businesses earning below this threshold, the tax remains at 0%, a measure aimed at supporting startups and small enterprises. This system applies consistently, regardless of the owner's nationality or residency, making it straightforward for businesses to navigate.

Saudi Arabia, on the other hand, employs a dual taxation model based on ownership structure. Foreign-owned profits are subject to a 20% corporate income tax, while entities fully owned by Saudi or GCC nationals are exempt from corporate tax. However, these entities must fulfil their Zakat obligation, a religious levy calculated at 2.5% of the Zakat base, which is determined by net worth or capital rather than profit.

UAE: 9% Corporate Tax and Free Zone Incentives

The UAE’s corporate tax framework is particularly advantageous for smaller e-commerce businesses. Many startups and growing online retailers fall within the 0% tax bracket, paying no corporate tax until their profits exceed AED 375,000. Even then, the 9% rate applies only to the portion of profits above this threshold, offering a graduated tax structure.

For businesses operating in Free Zones, the tax benefits are even more pronounced. Free Zone entities can enjoy a 0% corporate tax rate on "Qualifying Income", provided they meet specific substance and activity requirements to qualify as a "Qualifying Free Zone Person". This is especially beneficial for e-commerce companies engaged in cross-border trade or offering digital services outside the UAE mainland. However, all taxable entities, including those in Free Zones, must register for Corporate Tax and file returns within 9 months of the end of their tax period.

"The UAE's appeal lies in its relatively low tax rates, the possibility of tax exemptions in free zones, and a compliance system that is streamlined and transparent." - Choose UAE

Setting up a business in the UAE involves initial costs ranging from USD 2,700 to USD 18,900, with Free Zone licences starting at around USD 1,500. These lower setup costs, combined with the UAE's 0% withholding tax on cross-border payments like dividends, interest, and royalties, make it an attractive option for foreign investors.

KSA: 20% Corporate Tax and 2.5% Zakat

In Saudi Arabia, foreign investors face a 20% corporate income tax on their share of profits. For businesses with mixed ownership, tax obligations are split proportionately between foreign and GCC shareholders.

Saudi and GCC-owned entities, however, are exempt from corporate tax but must pay Zakat at 2.5% of their Zakat base. Unlike profit-based taxes, Zakat is calculated on net worth or capital, meaning businesses may owe Zakat even in years when they generate no profit. It’s worth noting that the UAE-KSA Double Tax Avoidance Agreement, effective since 1 April 2019, does not reduce Zakat obligations in Saudi Arabia.

"Saudi Arabia, while having higher tax rates in many cases, offers access to a large and growing consumer market, which can be a major advantage for businesses targeting the region." - Choose UAE

Establishing a business in Saudi Arabia comes with higher upfront costs, ranging from USD 13,000 to USD 40,000. A MISA (Ministry of Investment of Saudi Arabia) licence alone costs approximately USD 3,200, and businesses must also account for "Saudisation" requirements, which can increase operational expenses.

Corporate Tax Comparison

| Feature | UAE | KSA |

|---|---|---|

| Standard Corporate Tax Rate | 9% on profits > AED 375,000 | 20% on foreign-owned profits |

| Small Business Relief | 0% tax for profits ≤ AED 375,000 | Ownership-based |

| Religious Tax (Zakat) | Not applicable | 2.5% for Saudi/GCC-owned entities |

| Free Zone Benefits | 0% on Qualifying Income | Limited (mostly 0% in QFC/QFZA) |

| Tax Basis | Profit-based | Ownership-based |

| Filing Deadline | 9 months after tax period end | Monthly or quarterly (based on revenue) |

| First-Year Setup Costs | USD 2,700–18,900 | USD 13,000–40,000 |

For e-commerce entrepreneurs, the decision between the UAE and KSA often depends on ownership structure and profit expectations. GCC nationals may find KSA's 2.5% Zakat more appealing than the UAE's 9% profit tax, while foreign investors are likely to prefer the UAE's lower corporate tax rate over KSA's 20%. In the UAE, careful selection of Free Zone jurisdictions is crucial to securing the 0% rate on qualifying income.

These contrasting tax systems shape not only compliance strategies but also the broader cost structure for businesses, setting the stage for further financial planning and operational decisions.

sbb-itb-058f46d

Tax Compliance Challenges and Benefits

Introducing digital tax systems in the UAE and Saudi Arabia has created a mix of challenges and opportunities for e-commerce businesses. While the initial costs for technology and training can be significant, the long-term benefits often outweigh these investments. Let’s dive into the specifics of compliance costs, technical requirements, and how these systems are reshaping operations.

Compliance Costs and Technical Requirements

In the UAE, the government is shifting to a Peppol-based e-invoicing system. This requires businesses to work with an Accredited Service Provider (ASP) by set deadlines. Companies with revenues above AED 50 million must comply by 31 July 2026, while smaller businesses have until 31 March 2027. The process includes selecting an ASP approved by the Ministry of Finance to act as a gateway for the Peppol network and ensure invoices meet validation standards.

To stay compliant, businesses need to audit their IT and accounting systems. This may involve upgrading outdated systems or deploying entirely new platforms to generate machine-readable invoices.

Saudi Arabia, on the other hand, uses the FATOORA system, which follows a centralised clearance model. Here, invoices must be submitted to ZATCA for approval before being sent to buyers. Businesses must integrate their systems with ZATCA’s infrastructure, using UBL 2.1 XML formats and Cryptographic Stamp Identifiers (CSID) for digital signatures. This model applies to both B2B and B2C transactions, adding complexity for companies operating in multiple sectors.

"It is important for [micro-businesses] to have a level playing field by having access to the latest technology at an affordable price that creates an environment for automation and simplification."

- UAE Ministry of Finance

Smaller businesses face unique challenges. In the UAE, around 82% of businesses are micro-enterprises with annual revenues below AED 3 million. For these companies, the cost and complexity of compliance can be particularly daunting.

Fraud Prevention and Operational Improvements

Beyond meeting regulatory requirements, digital tax systems offer significant operational advantages. Automation enhances fraud prevention through encrypted transactions and real-time data tracking. This not only reduces the risk of errors but also improves cash flow and speeds up VAT return processes. With the Decentralised Continuous Transaction Control and Exchange (DCTCE) model, tax authorities gain near real-time visibility into transactions, making it easier to detect issues or fraudulent activity.

"E-invoicing is one such mechanism that has helped countries minimise such leakages [VAT leakage]."

- UAE Ministry of Finance

Standardised invoice formats and proactive data management further reduce errors during automated validation processes.

Challenges and Benefits Comparison

Here’s a quick comparison of the challenges and benefits for businesses in the UAE and KSA:

| Aspect | UAE | KSA |

|---|---|---|

| Implementation Timeline | Phase 1: Jan 2027; Phase 2: Jul 2027 | Fully implemented in waves |

| Technical Model | Decentralised (Peppol network) | Centralised clearance (FATOORA) |

| ASP Requirement | Mandatory for all phases | Not required (direct ZATCA integration) |

| Transaction Scope | B2B and B2G (B2C excluded) | B2B and B2C mandatory |

| Cost Reduction Potential | Up to 66% reduction | Similar automation benefits |

| Penalty for Non-Compliance | AED 5,000/month for system failure | Varies by violation type |

| Data Storage | Must remain within UAE | Local storage rules apply |

The UAE’s penalty structure highlights the importance of compliance. Businesses failing to implement the system or appoint an ASP face fines of AED 5,000 per month. Additionally, missing deadlines for issuing or transmitting invoices can result in penalties of AED 100 per document, capped at AED 5,000 monthly. If system failures occur, companies must report them to the FTA within two business days to avoid an additional AED 1,000 daily fine.

"By adopting eInvoicing, UAE government will have access to the relevant data in near real-time which will help in providing deep insights to policy makers for identifying areas and sectors that need government support."

- UAE Ministry of Finance

For e-commerce businesses operating across both countries, the differences in technical requirements mean separate integration strategies are essential. While the UAE’s OpenPeppol standard supports international invoice exchange, the KSA system is more focused on domestic transactions.

Future of E-Commerce Taxation in the GCC

GCC Tax Policy Alignment

The UAE and Saudi Arabia are making strides towards closer tax coordination, even though their systems remain distinct. Both have committed to the OECD's 15% global minimum tax for large multinational companies with revenues exceeding €750 million, setting a regional "tax floor" for businesses. While their VAT rates differ, both countries operate within a unified GCC framework.

The UAE's adoption of the OpenPeppol standard simplifies cross-border transactions, offering e-commerce businesses operating across Gulf states a unified digital framework for compliance. Recent regulatory updates highlight this alignment. For instance, Saudi Arabia has introduced new guidance on "deemed supplier" obligations for electronic marketplaces, effective January 2026. Meanwhile, the UAE has amended its tax laws to align limitation periods (five years) across VAT, Excise, and Tax Procedures laws. These changes aim to ease the administrative load for businesses operating in both countries.

A shift towards a Decentralised Continuous Transaction Control and Exchange (DCTCE) model is also underway, enabling real-time tax data reporting to authorities. This system could eventually harmonise across the GCC, making compliance simpler for businesses operating in the UAE and KSA. For the UAE's micro-enterprises - 82% of businesses with annual revenues under AED 3 million - these changes offer affordable access to automation tools, levelling the playing field in the cross-border market. These steps are setting the stage for technological advancements in tax administration.

Technology Advances in Tax Administration

Technological innovation is reshaping tax administration across the GCC, building on recent regulatory harmonisation. Tools like artificial intelligence and big data analytics are enhancing tax monitoring and fraud detection capabilities. According to an EY report, CFOs and tax leaders are leveraging AI to keep up with evolving regulatory demands. These technologies are becoming integral to the tax systems across the region.

The UAE's implementation of the PEPPOL network represents a significant leap forward. By using encrypted, decentralised data exchanges, it reduces the risk of unauthorised access. Automation within this system also minimises human intervention, helping to identify and address "VAT leakage" caused by errors or fraud.

E-invoicing is another game-changer, providing tax authorities with near real-time insights. This data-driven approach enables more precise government interventions and policy adjustments. The impact is already visible: by late 2025, over 651,000 companies in the UAE had registered for corporate tax, and nearly 34,000 businesses benefited from administrative penalty waivers during the initial corporate tax phase.

For e-commerce businesses, these advancements mark a shift from periodic tax reporting to a "Continuous Transaction Control" system, where tax data is transmitted to authorities almost instantly. To adapt, companies need to integrate their Enterprise Resource Planning (ERP) and accounting systems to meet the structured electronic format requirements. Unstructured formats like PDFs or scanned documents will no longer qualify as valid e-invoices. These upgrades not only improve efficiency but also address compliance challenges faced by e-commerce operators in the region.

Key Takeaways for E-Commerce Businesses

E-commerce businesses operating between the UAE and Saudi Arabia face distinct tax environments. In the UAE, companies deal with a 5% VAT and a 9% corporate tax, creating a relatively lighter tax burden. In contrast, Saudi Arabia imposes a 15% VAT, a 20% corporate tax, and an additional 2.5% Zakat specifically for GCC-owned entities.

When it comes to e-invoicing, each country has unique compliance requirements. Saudi Arabia mandates the use of the FATOORA system, which involves real-time, XML-based invoice clearance with ZATCA. Meanwhile, the UAE plans to implement a Peppol-based e-invoicing system by July 2026, requiring businesses to work with Accredited Service Providers. Additionally, VAT registration thresholds differ: the UAE enforces a threshold of AED 375,000, while Saudi Arabia requires all non-resident providers to register for VAT regardless of revenue. These differences highlight the need for tailored compliance strategies in each market.

To secure 0% VAT on cross-border sales, businesses must keep thorough export documentation, including customs declarations, airway bills, and proof of payment, for at least five years. For exports from the UAE to Saudi Arabia, goods must be shipped within 90 days to qualify for zero-rating. On the services side, B2B transactions typically fall under the Reverse Charge Mechanism, while B2C transactions are subject to a 5% UAE VAT.

Given the invoicing requirements, upgrading ERP and accounting systems is essential. These platforms should be capable of handling structured XML/UBL formats and offer seamless API integration with tax authorities. In Saudi Arabia, staying updated on ZATCA's monthly announcements is critical, especially as the revenue threshold for Phase 2 e-invoicing integration dropped to SAR 7 million in January 2025. In the UAE, businesses with revenue exceeding AED 50 million should start testing Peppol-compliant systems to meet the January 2027 deadline.

Tax treaties and free zone benefits also play a key role in shaping operations. The UAE-KSA Double Tax Avoidance Agreement, effective since 2019, ensures that corporate income is not taxed twice, although it does not exempt businesses from Zakat in Saudi Arabia. Additionally, businesses in UAE Free Zones can improve their tax positions by separating "Qualifying Income" (zero-rated for exports) from mainland sales, which are subject to a 9% corporate tax.

FAQs

How do VAT rates in the UAE and Saudi Arabia impact e-commerce pricing strategies?

VAT rates significantly influence how e-commerce businesses approach pricing in the UAE and Saudi Arabia. In the UAE, the VAT rate is set at 5%, whereas Saudi Arabia applies a higher rate of 15%. These variations have a direct impact on product pricing, profit margins, and consumer spending habits.

For businesses, integrating VAT into pricing strategies is essential to stay competitive and comply with local tax laws. This means ensuring invoices are accurate and tax reporting is precise to avoid any penalties. Companies operating in both countries must also account for how these differing VAT rates affect cross-border sales and shape customer expectations.

How do e-invoicing regulations differ between the UAE and Saudi Arabia, and what do they mean for businesses?

E-invoicing rules in the UAE and Saudi Arabia are quite different, which creates unique challenges for businesses operating in both countries. In the UAE, e-invoicing will be introduced in stages, starting in Q2 2026. The regulations, as outlined in Federal Decree-Law No. 16 of 2024, are designed to make compliance easier, enhance tax reporting, and cut down on administrative work. Companies will need to adopt systems that can produce structured, machine-readable invoices to meet these new standards.

Meanwhile, Saudi Arabia has already made e-invoicing mandatory. Since December 2020, businesses there must use approved systems to generate structured electronic invoices. These systems must comply with strict technical and procedural guidelines, and non-compliance can lead to penalties.

For businesses operating in both the UAE and Saudi Arabia, implementing strong digital invoicing systems is critical. This ensures compliance with each country’s regulations, supports smooth cross-border trade, and keeps tax reporting accurate.

What is the impact of corporate tax and Zakat on foreign e-commerce businesses in Saudi Arabia?

Foreign-owned e-commerce businesses in Saudi Arabia face two primary financial obligations: corporate tax and Zakat, both of which can have a notable impact on their operations and profitability. Corporate tax is set at 20% of the profits earned by non-Saudi entities operating in the Kingdom. This tax rate adds a layer of operational costs, making thorough financial planning a necessity. On the other hand, Zakat - a religious wealth tax - requires Saudi and certain foreign-owned businesses to contribute 2.5% of their Zakatable assets annually, further increasing their financial responsibilities.

These tax requirements play a significant role in shaping business strategies. Corporate tax, being profit-based, demands precise management of earnings and expenditures. Meanwhile, Zakat, calculated on assets, underscores the importance of optimising asset utilisation and revenue streams. Staying compliant with these regulations is not just about avoiding penalties but also about maintaining smooth and sustainable operations in Saudi Arabia's dynamic market.